Download the full report (pdf) here.

Welcome to the first quarterly report from the Big Blockchain Game List.

An outworking of 18 months of data collection from the List, our goal is to combine such data with other sources plus high quality analysis to provide contextualized insights into what’s happening in the blockchain gaming sector.

Notably, in conjunction with the report, much of this data is also displayed and manually updated with reasonable frequency at the Everything Blockchain Gaming sheet.

//What just happened?

With the price of ETH rising 52% during Q1 2024 and BTC up 65% – also hitting an all-time high of $73,738 on 14th March on the back of $12 billion of inflows from institutional and retail investors in the form of Bitcoin ETFs – it’s clear the crypto market is in full bull territory.

The situation for the blockchain gaming sector proved more nuanced however, with strong sentiment in January and February driven by token launches such as Heroes of Mavia‘s MAVIA and many play-to-airdrop events – notably for Pixels’ PIXEL token – lessening in March as wider crypto interest cycled into more speculative assets, notably Solana-based memecoins.

This isn’t to say game companies haven’t tried to ape into such sentiment. After prolonged social media shilling, the launch of so-called “universal gaming coin” PORTAL in late February was one such. The weakness of gaming in such a category is that the temptation to invoke utility becomes irresistible. But what’s a memecoin with a roadmap?

Thankfully, actual utility was the focus for some gaming projects during the quarter, with the most successful crypto-native investments involving the launch of scaling infrastructure and associated node sales. Examples include Xai’s Arbitrum-based L3, which raised $15 million in node sales (in December 2023), and Hytopia’s Arbitrum-based Hychain, raising $8 million. Gaming adjacent cloud-compute project Aethir raised over $65 million from its node sale.

Other projects talking up their efforts to launch similar tech include Proof of Play (Pirate Nation), TreasureDAO, Xterio and Wilder World. Brutally put, it’s now so simple to launch your own blockchain, most projects are at least considering it. Whether they need to do so is considered irrelevant given the current opportunity to use the situation to raise funds.

Notably, at this point it’s worth highlighting the power of a growing band of individual angel investors – we could impolitely label them the degen mafia – who are levering their social media muscle to highlight earning opportunities to their followers, while also maximizing their own ROI via valuable referral programs, which can deliver six figure rewards.

Aside from such considerations, however, there were teams demonstrating product-market-fit, with the quarter’s obvious winners being Sky Mavis’ Ronin blockchain and social RPG Pixels, which in becoming the most popular blockchain game, also propelled Ronin to an all-time high of 1.2 million daily active unique wallets.

On the back of this activity, other Ronin-based projects such as Apeiron, CyberKongz and Kaidro experienced a halo effect, notably in terms of their tokens’ value, although they are still early in their journey. Even veteran Yield Guild Gaming’s YGG token got a healthy boost from launching on Ronin.

The situation for other playable blockchain games was more complex, notably because while they are playable, their blockchain features are generally lightweight at best. Nevertheless, headline news from team shooter Nyan Heroes and strategy game Blocklords was they had each achieved over 100,000 downloads from the Epic Games Store, while extraction shooter Shrapnel has seen over 60,000 players across its two playtests.

More significant, perhaps, have been the claims that Big Time has generated $100 million in revenue since starting its pre-season event in October 2023, while Pixels‘ current monthly recurring revenue for its VIP program is running at $1.6 million.

As ever, it will be those projects that can combine playerbase and revenue with an overall vision and the delivery of new features, while wrangling the currents of crypto sentiment and the peculiarities of their own communities, that will be best placed for long term success.

//Onchain gaming activity

In a sector awash with data, finding significant data is often a challenge but when it comes to onchain game activity during Q1 2024, the clear winner was browser-based social RPG Pixels.

Originally launched on the Polygon blockchain, it relaunched in November 2023 on Sky Mavis’ Ronin chain, finding immediate success. Indeed, in part because of the decline of Alien Worlds and Splinterlands, Pixels has been the most popular blockchain game in terms of its daily active unique wallets since December.

But its hockeystick growth only began in January 2024. In part, this has been due to action the Pixels team has done, such as a play-to-airdrop event for the game’s new PIXEL token. Significantly, Pixels has also become a platform for other agents in the blockchain game sector, with Animoca’s Mocaverse collective driving its community to the game. More recently, guilds such as Yield Guild Gaming have become active, encouraging their communities to join them in-game to earn rewards both internal to the game and via the guild’s own programs.

Of course, this is very similar to how guilds drove the boom-bust success of Axie Infinity as a play-to-earn game in late 2021. The difference here is that Pixels has much better designed game loops and economy. Indeed, it is notable that despite its growing audience, Pixels’ PIXEL token isn’t experiencing any price volatility.

Yet it is starting to find real utility. For example, 160,000 players are now paying $10 a month in PIXEL to get VIP membership, generating recurring monthly revenue of $1.6 million for the developer, meaning Pixels is already operating profitably.

Hence, the interesting future question won’t be whether Pixels will break Axie Infinity’s one day peak of 1.1 million DAUWs – which aside from symbolism is irrelevant –

but at what level it can sustain its audience over the remainder of 2024.

//Token performance

Q1 2024 provided a strong environment for the launch of new tokens, although this hasn’t yet proven to be something particularly reflected in the gaming sector. For while the launch of gaming L3 Xai’s XAI token was successful for example, the launch of gaming memecoin PORTAL was not, demonstrating that this is not yet a tide that floats all boats.

Similarly, a number of gaming tokens declined in value during Q1, including Wemade’s WEMIX, Find Satoshi Lab’s GMT and TreasureDAO’s MAGIC, while large cap gaming cryptos such as The Sandbox’s SAND, Axie Infinity’s AXS and Apecoin’s APE only experienced a marginal rise in value.

Yet a number of newer tokens did hit their all-time highs during Q1, including Parallel Studios’ PRIME token, the BEAM token (although technically this is a reissued version of Merit Circle’s MC token), as well as Ronin’s RON token, which was launched way back in 2022.

Surprisingly, however, looking at tokens within the top 200 cryptos ranking, the best performer was Yield Guild Gaming’s YGG token, which launched back in 2021 at the height of the Axie Infinity boom.

The reason for its more-recent velocity was it went live on the buoyant Ronin blockchain, gaining liquidity and much lower transaction fees than available on Ethereum, where it had been previously available.

//Investment trends

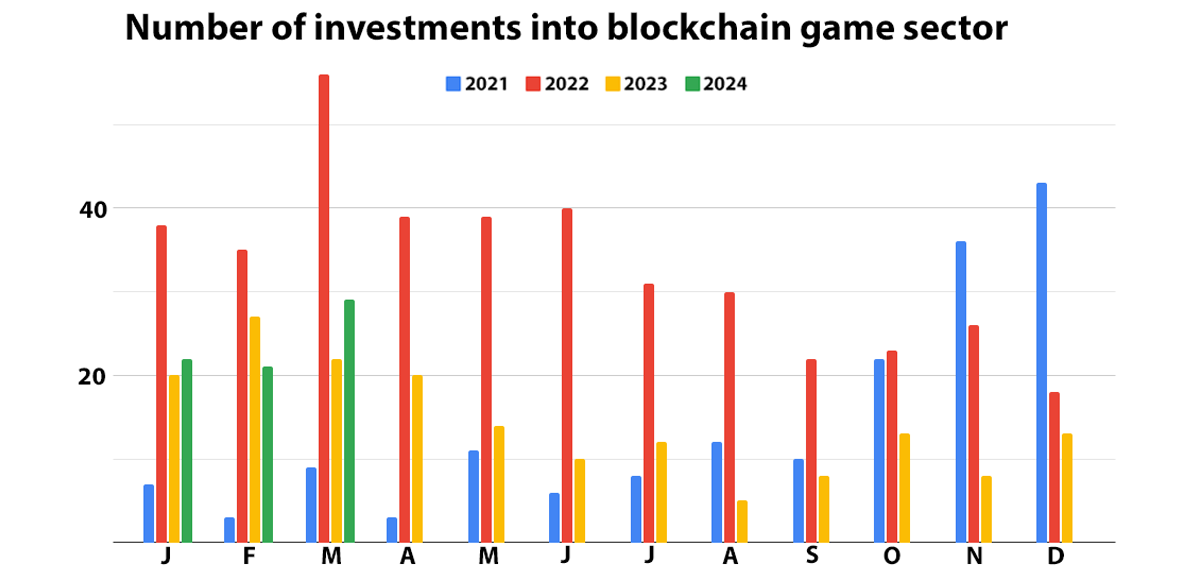

The first three months of 2024 saw 68 investment deals in the blockchain gaming sector, down 1% compared to Q1 2023 and down 57% compared to the boom times of Q1 2022 in which 56 deals were announced in March 2022 alone.

The majority of 2024’s activity was driven by interest retail crypto investors with token IDOs and node sales proving popular and in some cases generating instant returns. However, such retail activity is generally capped in terms of investment raised, typically accounting for low millions via token launchpads.

In terms of value invested, Q1 2024’s total of $301 million was down 39% compared to Q1 2023 and down 84% compared to the $1.9 billion announced in Q1 2022.

Two-thirds of this total was invested by professional VCs and investors, mainly crypto-only funds. In general, traditional tech and game VCs have not re-engaged with the sector following 2023’s wash-out, although there has been a stronger investor rebound across the entire crypto sector, especially scaling infrastructure.

Looking at specific deals in gaming, there were 24 investments worth more than $5 million, with seven deals worth $10 million or more.

.

Notably, many of these companies had already raised substantial investments, with Parallel Studios’ lifetime funding now being $85 million over two funding rounds, Gunzilla Games over $100 million over seven rounds, and Illuvium over $125 million across three funding rounds and multiple NFT and token events.

The spread of investor participation was broad, however, with over 260 named individuals and entities participating.

The most active investors during the quarter in terms of public announcements were:

- Spartan Capital – 7 deals

- Animoca Brands – 7 deals

- Sfermion – 6 deals

- Merit Circle – 5 deals

- Delphi Ventures – 5 deals

- Yield Guild Gaming – 5 deals

- Cypher Capital – 5 deals

In terms of lead investors, the most active were:

- Framework Ventures – 3 lead deals

- Animoca Brands – 2 lead deals

- Delphi Digital – 2 lead deals

Notable angel investors included:

- Gabby Dizon (YGG) – 4 deals

- Alex Becker (Neo Tokyo) – 4 deals

- Dingaling – 3 deals

//Ecosystem trends

As ever, the Big Blockchain Game List has been tracking broad ecosystem trends as they relate to announcements around games and the blockchains they are deploying on.

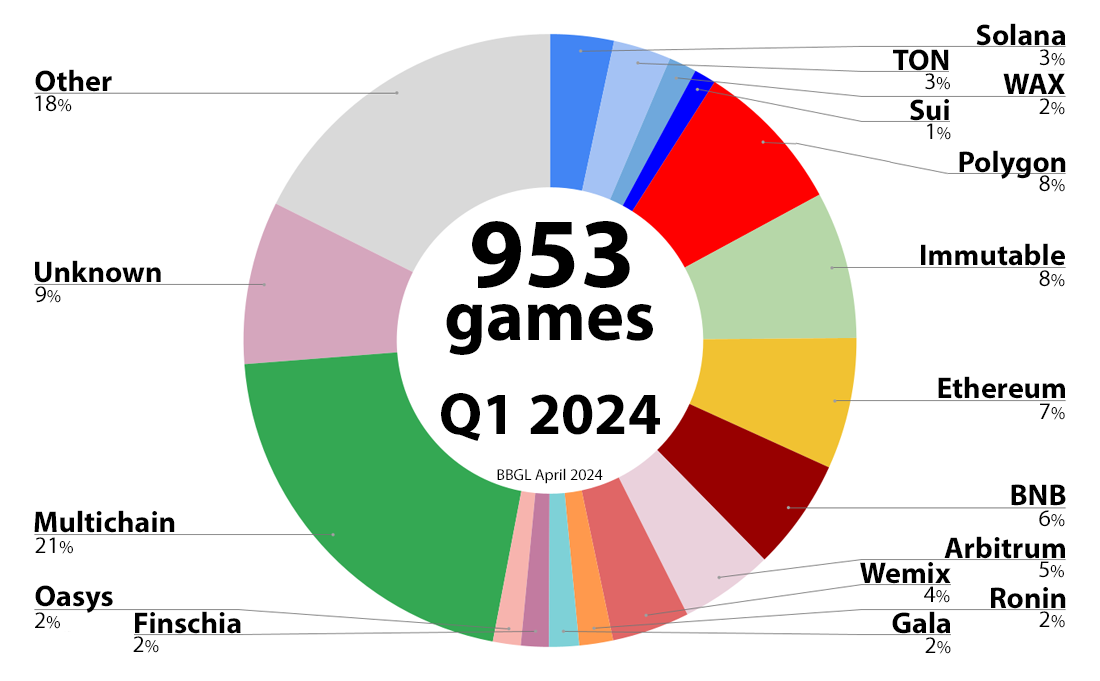

During Q1 2024, 119 new titles were added to the list, with Immutable proving the most popular destination in terms of a single blockchain. Of course, this isn’t a surprise as Immutable is gearing up for the launch of its Polygon-based Immutable zkEVM infrastructure, and hence is attracting a lot of inbound interest, as well as games migrating from Polygon’s legacy PoS blockchain.

Other popular designations include Ethereum L2s Arbitrum and Blast, the latter which supercharged activity with its highly rewarded Big Bang competition that attracted over 3,000 builders to launch apps and games on the high profile chain.

However, it’s also worth pointing out that the vast majority of games – 27% – are now taking a multichain approach, mainly in terms of expanding addressable audience.

In contrast to newly announced games, the single chains losing the most games during the quarter were Solana and Polygon.

As the tracking of discontinued games is an imprecise and lagging indicator, it’s likely that the data captured here reflects the relative weakness of both the Solana and Polygon ecosystems during 2023. As ever, there are always more blockchain games in development and looking for funding than the market can sustain so this level of discontinued product is not a surprise.

If anything, the surprise is that the attrition rate isn’t higher. For example, we noted 410 games discontinued in 2023, so 2024’s rate to-date reflects the sector’s improving sentiment.

Combining all this data, the Big List ended Q1 2024 tracking 953 blockchain games. This compares to a total of 896 games at the end of 2023, 824 games at the end of June 2023, and 724 games at the end of January 2023, demonstrating continued strong net growth even through the 2023 bear market.

Once again, the largest single category is games operating across multiple chains, which is up from a total 17% at the end of 2023.

In terms of single chains, Polygon and Immutable are top, although as previously stated, Polygon is currently declining the most, while Immutable is growing the most. It is worth restating that this trend is mainly just optics, however, as Immutable is onboarding games to its zkEVM infrastructure, which runs Polygon’s zkEVM blockchain under-the-hood.

The more significant trend is the continuing decline of non-EVM blockchains such as Solana,Ton, Sui, Wax etc, which now consists of under 10% of all blockchain games. Indeed, many of these blockchains are now deploying EVM-compatibility.

As for other blockchains, Arbitrum continues its growth in part to the flexibility it offers, particularly for developers to use its tech to deploy their own infrastructure.

Gala remains very quiet in terms of new product, while Ronin is steadily announcing more games. After a very busy 2023, Wemix appears to be focusing on quality not quantity with the launch of its MMORPG Night Crows being the classic example. Similarly, the key launch for Japanese gaming blockchain is Ubisoft’s Champions Tactics, while the big news for Line Next’s Finschia will be its forthcoming merger with Kakao’s Klaytn.

Download the full report (pdf) here.

One response to “Big Blockchain Game Report: Q1 2024”

[…] 2024 年第一季度 这里,和/或 在此下载 pdf […]

LikeLike